Client Alert – SEC Pay Versus Performance Disclosure Rules

By Elyse HoffmannPublished On April 26, 2023

The SEC announced its new rules regarding pay versus performance disclosure requirements on August 25, 2022. These rules were mandated by Dodd-Frank and the Consumer Protection Act almost 13 years ago. The new rules (Item 402(v) in the proxy statement) will be implemented in the 2022 proxy statements that will be developed during the 2023 proxy season (specifically, fiscal years ending on or after December 16, 2022).

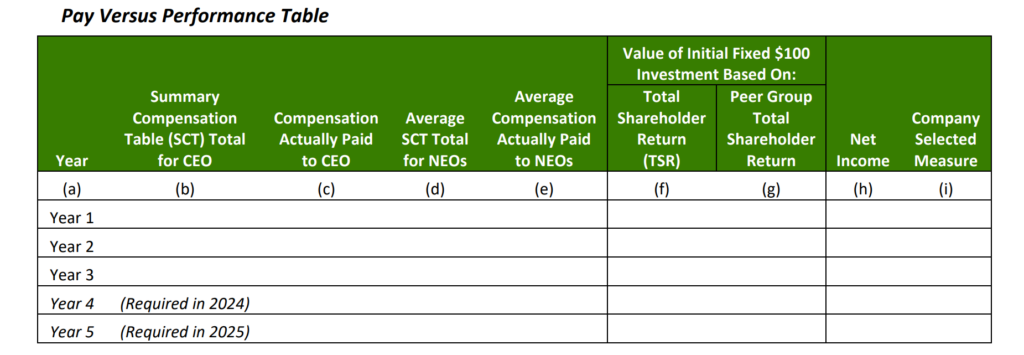

The full guidance can be found on the SEC site here: Pay Versus Performance Final Rules and they also provide a Fact Sheet as well. The new disclosures will require a new pay versus performance table and the associated disclosures, along with a list of three to seven financial performance measures that the Company feels are its most important.

Key Table Considerations

How to Calculate Compensation Actually Paid (CAP): This will differ from the Summary Compensation Table (SCT) amounts by the following:

Change in Pension Value Adjustments: Instead of SCT values, this table will instead be reflective of the “service cost” for the appropriate year (excluding changes due to interest rates, age, and other actuarial assumptions) plus the additional service cost of any amendments during the current year that impacts prior year service costs.

Change in Equity Values: Instead of the SCT values, which focus on the grant date fair value of stock and option-based awards, the equity value will be reflective of the following: 1. Awards granted in the current year: The fair value of these equity awards as of fiscal year-end if unvested or the fair value at vesting date if the equity grant vests during this same year. 2. Unvested awards granted in prior years: The year-over-year change in the fair value from the end of the prior fiscal year through the current fiscal year-end. 3. Awards vesting in the current year that were granted in prior years: The year-over-year change in the fair value from the end of the prior fiscal year through the vesting date. 4. Dividends: The actual amounts paid to the executive.

Peer Group Selection: The Company can use either the peer group utilized under Item 201(e) of Reg. S-K (stock price performance graph in the 10K) or the compensation benchmarking peer group as disclosed in the Compensation Discussion & Analysis (CD&A).

Company Selected Measure: This is the most important financial measure (as chosen by the Company) that relates to executive pay.

Other Key Items

Small Reporting Companies (SRCs): SRCs will have reduced disclosure requirements. An example is the SRCs do not have to disclose a peer group TSR value and do not have to provide the key performance metric tabular list (see below).

Key Performance Metric Table: Companies need to provide a tabular list of three to seven measures that are considered the most important measures in determining CEO and NEO pay. At least three measures must be considered financial metrics. Different metrics can be used for the CEO and each NEO.

Disclosures: There is a requirement to disclose the relationship between CEO and NEO Compensation Actually Paid (CAP) amounts versus Company TSR, Company Net Income, and the Company Selected Measure. These relationships need to be disclosed by either a graphical or narrative approach. Additionally, a discussion surrounding the Company TSR versus the Peer Group TSR will be required.

Next Steps If you are a public SEC filer, there will be some additional work to do related to this new disclosure requirement. We provide a list of items that you’ll want to be thinking about below.

Determine who will be assisting with this new disclosure and the related elements. This will generally include your internal proxy team, your SEC counsel, and your compensation consultant.

Identify the executives that will be included in the pay versus performance disclosures and start to calculate 2020 and 2021 CAP data along with the TSR data for prior years.

Begin discussions surrounding the peer group that will be utilized for the TSR calculation.

Determine the one Company selected measure to include in the table and the three to seven performance metrics that will be disclosed as the most important related to NEO pay.

Strategize on the narrative and/or graphical discussions surrounding the disclosure and determine the proxy placement of these disclosures.

Create draft tables and disclosures and establish a timeline for completion of this work.

It has certainly taken some time, but the pay versus performance rules are finally here. Blanchard Consulting Group will be helping our clients develop these proxy related disclosures in early 2023. We will continue to fine-tune our processes and insights over the next few months. If you have any questions about this client alert, please contact us at info@blanchardc.com.